Beginner’s Series - Part 3 of 4

In this 4-part series, you’ll learn everything you need to navigate this site and begin earning your way to free credit card points

Manufactured Spending Deep Dive

This is the third post in our series on manufactured spending for beginners. Previously, we covered key concepts behind manufactured spending, and answered some basic questions related to the hobby. Here, we will (1) cover real step-by-step examples of manufactured spending and (2) provide a timeline that you can reference.

A land of riches awaits you!

Basic Principles

The basic principles of earning credit card points from manufactured spending comes down to two simple steps:

Find a reward play (e.g. spend $5K on card X to earn 100K points)

Manufacture spend on the card to earn your reward (e.g. manufacture $5K of spend)

Let’s take a closer look at both of these steps.

Step 1: Finding a reward play

A classic reward play for beginners

A reward play may sound daunting by name, but it’s just when a credit card offers a reward for spending some amount of money on a card. Finding a reward play doesn’t have to be hard - in fact, we maintain a list of our current favorite reward plays.

These generally fall into two categories: Spending-based and category-based.

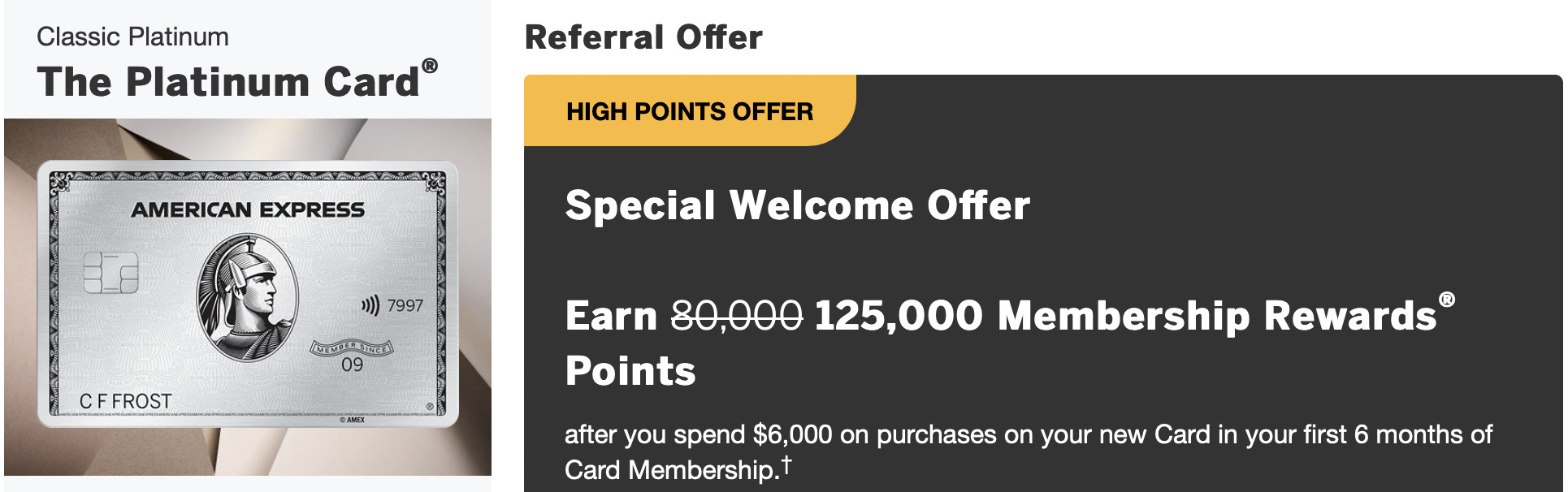

Spending-based

Spending-based plays typically take the form of sign-up bonuses - You will sign-up for a new credit card, and earn some enticing amount of points for spending some amount of money. The screenshot above shows an example of this on the Amex Platinum card. At any point in time, almost all credit card companies will be offering some type of sign-up bonus for their cards. This type of spending does not have to conform to any specific category.

Category-based

Sadly the best thing that happened to me in 2023

Other common reward plays involve some type of spending within a specific category, in return for some multiplier bonus on your spend. For example, in 2023, Amex offered a reward of +5X on every dollar spent at grocery stores, up to $25,000 in spend. If you got this reward on the Amex Gold card, which already earns 4X on grocery stores, you would have earned 9X (4X+5X) on grocery spend. If you played this perfectly, this would have earned you 225K MR points ($2,250 if directly cashed out).

Common Questions around reward plays

-

Yep, you can definitely do that. Manufactured spending is for folks who don’t want to spend their “real” money towards earning these rewards. If you’re content with opening a card or two a year and applying your real spending towards the card to earn rewards, go for it! Generally, the higher the amount of spending needed to earn a reward, the bigger the reward will be.

On the other hand, if you want to earn a ton more points while costing you little to no money, this hobby may be for you!

-

Yes, most cards have an annual fee, ranging anywhere from $50 - $650. Most of these cards have benefits that outweigh the cost of the card, assuming you can fully utilize those benefits. If you are opening cards purely for a sign-up bonus, you should typically downgrade or close the card as soon as the first year is over. Then, depending on the card, you can sign-up for it again sometime down the line to earn the sign-up bonus all over again.

For more info on closing/downgrading a card, see this helpful post.

-

Valid concern! Yes, your credit score could be negatively affected if you are not careful. On the other hand, if you correctly follow the methods in our guides, your score will actually increase over time! Lets take a look at each action you might take, and how it would impact your score:

Opening a new credit card

While opening a new card will initially ding your credit score due to a hard pull, the negative impact will eventually be outweighed by the longer-term positive impact of having a larger amount of credit. For more on this, read this CNN article.

Carrying a high balance on your credit card

With manufactured spending, you may be putting large volumes on spend on your card. Your credit utilization ratio is an important factor in your credit score, which looks at what percentage of your total available credit you have used up. Hence, if you have a $10K credit limit and your statement shows you using $9K of that limit, you will have a 90% credit utilization ratio.

Having a high credit utilization ratio every once in a while is not a big deal. This is not a permanent demerit on your credit report, since the utilization ratio is recalculated monthly. To avoid these situations, I generally pay off my balances on my credit cards before the statement is generated. This prevents my cards from having a high utilization ratio, despite spending a large percentage of my available credit. For more details on this topic, read this helpful post from SmartAsset.

Paying off your credit card statements

As long as you pay off your credit card statements in full each month, your credit score will be unaffected. If you take anything away from this hobby, it is this: DO NOT SPEND MORE THAN YOU CAN AFFORD TO PAY OFF. Always pay off your credit card statements in full. In this hobby, there is a never ending supply of rewards to be earned. Makes sure you take things slow, and always have enough cash sitting by to pay off your credit card statements.

Downgrading a card

For most cards that you open purely for sign-up bonuses, you will want to eventually get rid of after the first year. Most cards with an annual fee can be downgraded to a lower-tier card with no annual fee. Downgrading is preferred to closing a card, since it will continue to positively impact your credit score, at no cost to you.

Closing a card

The only credit impact from this is that your available credit will go down, which can impact your credit utilization ratio. For those of us who already have a bunch of credit cards, our credit utilization ratio will be minimally impacted by any single card being closed. For more on this, check out this post from CNN Finance.

-

You can always look at our list of maintained reward plays at any time.

If you’re starting out, I suggest dipping your toes in with a sign-up bonus for a credit card with a low annual fee and a low spend requirement.

Once you feel comfortable with the process of manufactured spending, I suggest thinking of reward plays in terms of hourly earnings - for every hour you spend on this hobby, how much money/points are you earning? At the end of the day, we want to spend our time working on the most lucrative offers!

In general, to calculate this, we should consider the following simple equation:

(Rewards earnings - Fees towards earning) / Hours spent towards earning

Soon we’ll be adding an online tool for calculating your hourly earnings.

Take a look at our examples below to see this in practice.

Step 2: Manufactured Spending

Now for the fun part! Once you’ve picked a reward play, you will have some amount of money that you need to spend on your credit card. You may have a specific category that you need to spend on. We list all of our favorite manufactured spending methods here.

From here, this is a 1+ step process of converting money from your credit card into a bank account. Each method has different pros and cons, and typically will have some small percentage fee. We use the bonus earning calculator to make sure our rewards far outweigh any fees. There are a variety of methods to do manufacture spend, but some common methods include:

1 Step Methods

Funding a bank account with a credit card

Purchasing a CD with a credit card

Purchase electronics and ship them to reselling groups

Making a short-term loan with a credit card

Gift card liquidation methods

Purchase a Visa / Mastercard gift card (online, at the grocery store, etc), then liquidate it by:

Using it to buy a Money order, which you can deposit into your bank account.

Fund an investment account with your gift card, which you can cash out to a bank account

Load the gift card onto a reloadable debit card, which you can liquidate in various ways (e.g. bill payment services)

See the full list of our manufactured spending methods on this page.

Common Questions around manufactured spending

-

Fees can vary, but are typically in the 0%-3% range. Often there is a tradeoff between convenience/scalability and fees.

-

Why do I need to buy a gift card first, can’t I directly buy a money order / fund investment account / etc with my credit card?

-

You can absolutely focus on plays from home. In fact, I generally prefer plays that I can do from home, and am willing to take on a higher fee for that convenience.

Example: Earn $600 in value in 1 hour

Rewards Play: 60K Sign-up bonus (SUB) on Chase Sapphire Preferred ($600 value)

Manufactured Spend Method: Funding a bank account

Cost/Fees: $0

Steps

Open a Chase Sapphire Preferred card with a 60K sign-up bonus. I like looking for card referrals on Rankt, where you may be able to find further elevated offers.

Once you have your card, find a bank account that accepts credit cards for funding. The best place to find such banks accounts is on Doctor Of Credit. Especially take advantage of the comments at the bottom, which will have people’s most recent data points. You may need to fund multiple bank accounts to hit your sign-up bonus.

My favorite is GESA credit union, which let me fund $10K from a credit card, but this is limited to certain states.

Once your money is in your bank account, use it to pay off your credit card bill.

Approach analysis

Pros

Hourly earning rate is incredible ($600/hr)

No fees involved

Done completely virtually

Cons

Not scalable - Bank accounts can only be funded with a credit card when the account is first opened. If you wanted to do this again, you would need to find a new bank account. And unfortunately, there are only a limited number of banks that allow funding via CC. So you can only use this MS method a few times until you’re tapped out.

Some banks only allow limited amounts to be funded via CC, in which case you would need to open multiple bank accounts. This adds to the overhead of keeping track of multiple separate accounts.

Beginner's Manufactured Spending Schedule

Ready to finally start on your manufactured spending journey? Hop on to the next page to see a personalized month-by-month beginner’s guide to manufactured spending.